CBDT Announces New Scheme to Settle Pending Income Tax Litigation

The main objective of the new scheme is to reduce the enormous backlog of over 5.4 lakh appeals, involving disputed tax amounts exceeding Rs 10.6 lakh crore.

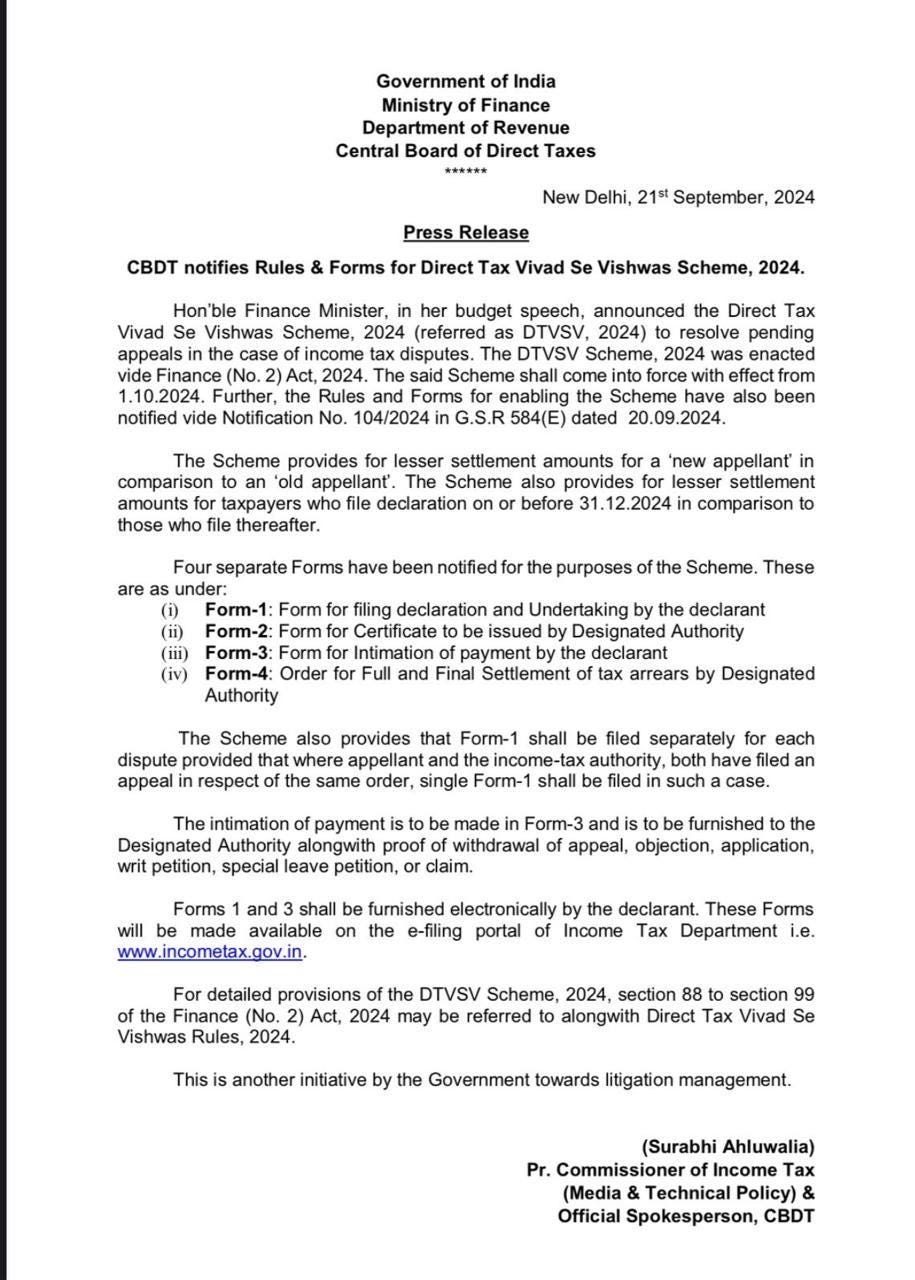

Direct Tax Vivad Se Vishwas Scheme, 2024 (विवाद से विश्वास योजना, 2024) Announced

Following the issuance of statutory notification No. 104/2024 in G.S.R 584(E) dated 20.09.2024, the Central Board of Direct Taxes (CBDT) has officially introduced the Direct Tax Vivad Se Vishwas Scheme, 2024 (प्रत्यक्ष कर विवाद से विश्वास योजना, 2024). Announced by the Hon'ble Finance Minister during the Union Budget, the scheme is aimed at resolving long-pending income tax disputes. Building upon earlier frameworks, this new scheme includes key improvements that streamline the dispute resolution process, making it more efficient and effective. The main objective of DTVSV 2024 is to reduce the enormous backlog of over 5.4 lakh appeals, involving disputed tax amounts exceeding Rs 10.6 lakh crore.

The scheme applies to appeals pending as of 22nd July 2024 across various forums, including the Supreme Court, High Courts, Income Tax Appellate Tribunal, and Commissioner (Appeals). It provides taxpayers with an opportunity to resolve their disputes by paying a specified amount of tax, with many cases benefiting from waivers on interest and penalties. However, certain cases, such as those involving search and seizure (popularly called raid cases) or undisclosed foreign income, are excluded from the scheme. This initiative aims to facilitate swift resolution of disputes, easing the burden of litigation for both taxpayers and authorities.

Key Features

Scheme Implementation

The DTVSV 2024 will come into force from 1st October 2024, as enacted under the Finance (No. 2) Act, 2024, providing taxpayers an option to settle their tax disputes with a reduced financial burden.

Appellant Categories and Settlement Amounts

The scheme introduces two key categories:

New Appellants: Offered lower settlement amounts than older appellants, encouraging quicker dispute resolution.

Early Filers: Taxpayers who file declarations by 31st December 2024 receive lesser settlement amounts than those filing later, promoting prompt participation.

Documentation and Process

The scheme mandates four forms for the settlement process:

Form-1: For filing a declaration and undertaking by the declarant.

Form-2: For certification by the Designated Authority.

Form-3: For notifying the payment made by the declarant.

Form-4: For the final settlement of tax arrears by the Designated Authority.

Form-1 must be filed separately for each dispute, unless both the appellant and the income-tax authority have filed appeals for the same order, in which case only one Form-1 is needed.

Electronic Submission

Forms 1 and 3 must be submitted electronically via the Income Tax Department's e-filing portal (www.incometax.gov.in), streamlining the process for taxpayers.

Payment and Appeal Withdrawal

The payment must be reported in Form-3, along with proof of withdrawal of appeals or claims, to the Designated Authority.

Legal Framework

The detailed provisions are outlined in sections 88 to 99 of the Finance (No. 2) Act, 2024, along with the Direct Tax Vivad Se Vishwas Rules, 2024.

Critical Analysis

Potential Benefits

Litigation Reduction: The scheme has the potential to significantly reduce the backlog of pending tax litigation, freeing up resources and reducing administrative pressure for both taxpayers and tax authorities.

Revenue Collection: It presents an opportunity for the government to expedite the collection of disputed taxes, thereby improving cash flow and bolstering fiscal health.

Taxpayer Relief: By offering waivers on interest and penalties, the scheme provides taxpayers with a cost-effective way to settle long-standing disputes, reducing their financial burden.

Clarity on Tax Positions: The scheme allows taxpayers to achieve certainty regarding disputed tax positions without the need to concede their stance entirely, offering a clear resolution path.

Potential Drawbacks and Concerns

Fairness Issues: The scheme might be perceived as unfair by taxpayers who have already complied and paid their taxes in full, as they do not benefit from the waivers offered to those settling disputes.

Moral Hazard: The repeated introduction of such schemes (following the 2020 version) could encourage non-compliance, with taxpayers potentially delaying payments in anticipation of future settlement opportunities.

Complex Rules: The intricate rules and calculations involved in the scheme may lead to confusion, making the process cumbersome and increasing the likelihood of disputes during implementation.

Limited Time Window: The short timeframe for participation (until December 31, 2024, for maximum benefit) could rush taxpayers into decisions without adequate time for analysis, leading to hasty and potentially suboptimal choices.

Exclusions: Certain categories of cases, such as those involving search and seizure or undisclosed foreign income, are excluded from the scheme, which limits its overall reach.

Implementation Challenges

Form Complexity: The required forms (Form 1-4) necessitate detailed and precise information, which could be burdensome for taxpayers to compile, especially for those with multiple disputes.

Technological Readiness: The success of the scheme is contingent upon the smooth operation of the e-filing portal for submitting forms and making payments. Any technical issues could hinder the process and frustrate participants.

Interpretation Issues: There may be ambiguities in some of the rules, particularly concerning cases where the appeal time limit has not yet expired, which could result in further disputes.

Administrative Burden: Tax authorities will be required to handle a high volume of declarations within a short period, potentially straining their resources and leading to delays in processing.

Is DTVSV 2024 an Amnesty Scheme?

Arguments in Favour

Waiver of Penalties and Interest: Like many tax amnesty programs, the Direct Tax Vivad Se Vishwas Scheme, 2024 (DTVSV 2024) offers waivers on penalties and interest, incentivising taxpayers to settle disputes quickly. This is a hallmark feature of most amnesty schemes, providing financial relief to encourage compliance.

Limited Time Offer: Similar to typical amnesty schemes, DTVSV 2024 is a time-bound initiative. The limited window for participation pushes taxpayers to act swiftly, mirroring the short-term nature of amnesty programs that drive quick resolution of disputes.

Forgiveness in Exchange for Payment: The scheme allows taxpayers to settle disputes by paying a specified amount, which aligns with the core principle of amnesty programs where forgiveness of liabilities is granted in exchange for partial payments.

Revenue Generation Objective: One of the main goals of DTVSV 2024 is to rapidly collect disputed taxes, much like tax amnesty programs that aim to boost government revenue by recovering taxes that might otherwise be lost in prolonged litigation.

Encouragement of Compliance: By offering a pathway to resolve disputes with financial incentives, the scheme seeks to bring non-compliant taxpayers into the system, a common objective of tax amnesty initiatives.

Arguments Against

Focus on Disputed Cases: Unlike broad-based amnesty programs that typically target undeclared income or tax evasion, DTVSV 2024 is specifically designed to resolve pending tax appeals and litigations. This focus on disputed cases distinguishes it from general amnesty programs.

No Blanket Forgiveness: While amnesty schemes often provide full forgiveness of tax liabilities, DTVSV 2024 requires the payment of a specified amount. It does not offer complete absolution of tax dues but provides a structured settlement process.

Litigation Management Tool: The primary objective of DTVSV 2024 is to manage and resolve ongoing tax litigation rather than providing broad relief for tax non-compliance. This positions it more as a litigation resolution tool than a traditional amnesty program.

Differential Treatment: The scheme treats "new" and "old" appellants differently, which is not a common feature in general amnesty schemes. This differential treatment suggests a more nuanced and targeted approach, setting it apart from broader tax forgiveness initiatives.

Exclusions: Certain cases, such as those involving undisclosed foreign income, are excluded from the scheme. This makes DTVSV 2024 less comprehensive compared to typical amnesty programs, which often cover a wider range of tax disputes.

The role of Income Tax Advocates and Chartered Accountants

In this context, the role of Income Tax Advocates and Chartered Accountants will be crucial. Although these professionals may lose clients once litigation is conclusively resolved, they must approach their responsibilities with integrity and the highest levels of professionalism. Their primary duty will be to guide clients in navigating the scheme properly, ensuring they make the best use of the opportunity to resolve disputes and shift their focus back to business, rather than being burdened by crippling tax litigation.

The success of the Direct Tax Vivad Se Vishwas Scheme, 2024 (DTVSV 2024) will depend heavily on their initiative and cooperation. In parallel, the field formations of the Income Tax Department will need to work in tandem with these professionals to ensure that the scheme achieves its desired objectives. While DTVSV 2024 shares some features of tax amnesty programs—such as the waiver of penalties, limited participation, and revenue generation—it is primarily a targeted dispute resolution mechanism. Its success will rely not only on effective implementation but also on its long-term impact on tax compliance and the integrity of the tax system in India.

Previous Initiatives—Vivad Se Vishwas Scheme 2020

A similar scheme, the Vivad Se Vishwas Scheme 2020 was launched to settle direct tax disputes pending as of January 31, 2020. It aimed to expedite dispute resolution by allowing taxpayers to resolve cases through reduced tax payments, waiving penalties and interest.

Outcome:

By November 2020, 45,855 declarations were filed, reflecting considerable participation. Although data on total tax collection was not readily available, the scheme was regarded as relatively successful, prompting the introduction of a similar framework in 2024. Its success indicated that such schemes could help clear a backlog of cases and improve revenue collection, but the extent of dispute resolution remains uncertain.

Sabka Vishwas (Legacy Dispute Resolution) Scheme 2019

The Sabka Vishwas Scheme, introduced in 2019, focused on settling indirect tax disputes. This initiative targeted recovery from past tax disputes, particularly those related to service tax and excise duty.

Outcome:

The scheme surpassed its target, collecting over Rs 38,000 crore, exceeding the government's initial expectation of Rs 35,000 crore. Despite meeting its financial objectives, the scheme only partially achieved its broader goal of resolving a high number of disputes. The marginal success in dispute resolution indicated that while these schemes were effective for short-term revenue generation, they may not fully address the root causes of tax litigation.

Looking Beyond this Scheme— the New Income Tax Code

The DTVSV 2024 scheme offers a valuable opportunity to reduce the backlog of tax disputes and enhance the ease of doing business in India. However, its success hinges on clear communication, efficient execution, and addressing fairness concerns to ensure broad participation. While it provides short-term relief by resolving disputes, the government must also consider the long-term impact on tax compliance.

In this context, the new Income Tax Code, announced by the Hon'ble Finance Minister during the Budget session, holds great promise. It is expected to simplify the tax system, eliminate ambiguities, and prevent future litigation of this kind. The aim is to ensure that the right amount of tax is paid by the right people at the right time, fostering a more transparent and efficient tax regime. The new code should also enforce stricter penalties on tax evaders, deterring non-compliance and ensuring fairness. Structural reforms like these will be essential to complement the temporary solutions offered by schemes like DTVSV 2024 and to create a long-term environment of compliance and accountability in the tax system.

…….hoping & praying for similar like initiative to drastically reduce/finish pending court cases in the country so as to give justice to the hard pressed litigants……!!